A Guide to Blockchain : What is it, How It Works and Why It Matters

A Guide to Blockchain : What is it, How It Works and Why It Matters

Understanding the building blocks of blockchain - the technology that is driving the crypto revolution.

Cryptocurrency is the hottest topic in moneytown. The digital currency is dominating the discourse in finance, economics and markets with huge amount of information flow. In this issue, I explain how blockchain works. As usual, this article is only for information purpose only and not financial recommendation of any kind.

The Metro is a free newsletter on global business and technology news and views

The History of Blockchain

On 31 October 2008, a mysterious entity which goes by the pseudonym ‘Satoshi Nakamoto’ published a white paper titled “Bitcoin: A Peer-to-Peer electronic cash system” on a cryptography mailing list. This was the beginning of bitcoin and the creation of the first digital currency. The core or the engine which drives this technologically sophisticated and efficient system is blockchain.

The first person to propose a blockchain-like structure or protocol was a cryptographer named David Chaum. He published a dissertation in 1982 named “Computer Systems Established, Maintained, and Trusted by Mutually Suspicious Groups". There have been many further works on this concept by various mathematicians and cryptographers. But it was first conceptualized by ‘Satoshi Nakamoto’ when they developed bitcoin. Blockchain itself is based on the principles of cryptography. Cryptography is a set of mathematical techniques and methods which enables one to secure information and communication through the use of codes. This is exactly what a blockchain does.

What is blockchain?

Blockchain is basically a database which records and stores information. Like any other database, blockchain stores a large amount of information or data on a computer system which is accessible to a large number of users who can perform specific functions with the data. In most secured databases, the control is centralized. This means though users may have access to the database, the flow of information or data is controlled by a central authority which designs the rules which describe the use of information or data contained and has jurisdiction over user actions. Thus, the central control determines who can be a user or who can access the information in the database and how new information is registered. Many users simultaneously enter new information into the database or update existing data and the final or official record which is available to all the users is the one approved by this central authority.

But blockchain is fundamentally different from centralized databases in the way it stores and distributes the information. Any user can register new information on a blockchain network which is accessible to all. Now, this information is available to every node (the computer systems which are participants) in the blockchain network. The new information entered into the blockchain is recorded as legitimate only when the participants of the network authorize it to be so in accordance with an established protocol which is the computer program (more about how this is done in a bit). So every node in the network has access to the information and can simultaneously update or register new information with the most popular one being the final or official record. There is no single central authority or control which governs the flow of information. This is what makes blockchain a revolutionary technology. A blockchain network facilitates the building of digital relationships based on trust without any central third-party. We will try to understand how this extraordinary feat is achieved but before that a bit more on what exactly constitutes a blockchain.

Is blockchain a new invention?

Okay, so let’s go back into a bit of history, this may sound boring but it is essential to understand how a blockchain works. The blockchain, though one of the most sophisticated technologies in the modern world is not an entirely new concept. The blockchain is a result of a combination consisting of three already existing technologies. Blockchain is made up of three elements:

1) Private Key Cryptography - The use of a set of codes and numbers to secure information which enables transacting parties to be pseudonymous, that is, reveal only the essential details of their identity. This element is responsible for authentication of transactions.

2) Peer-to-Peer network - A network of computer systems on the same server which forms the core structure of a blockchain network architecture and is responsible for authorization of transactions.

3) The Blockchain Protocol - The computer program which defines the how the system will authenticate and authorize actions on the blockchain network.

These three elements work together to form an elegant, efficient and secure system to build digital relationships without any central third-party to validate the trust between the two transacting parties. Now, lets see how this works.

How a blockchain works?

To understand how a blockchain works, let’s consider a hypothetical function which needs to be performed- suppose an electronic financial transaction between two parties. How does a blockchain perform this function? Now, for any financial transaction the two most essential elements required are - authorization and authentication. Authentication ensures the identity of the two transacting parties, that is, the money is sent to the right entity by the right entity while authorization ensures that the transaction carried out by the two parties is a legitimate transfer of value and record it.

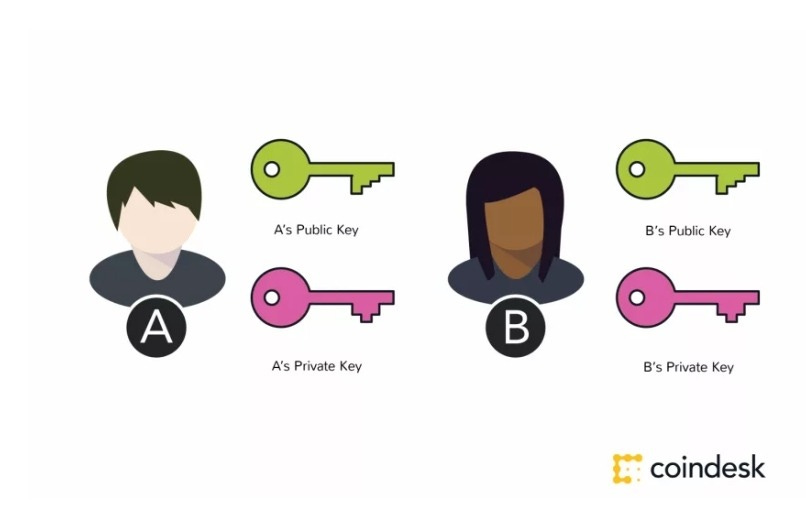

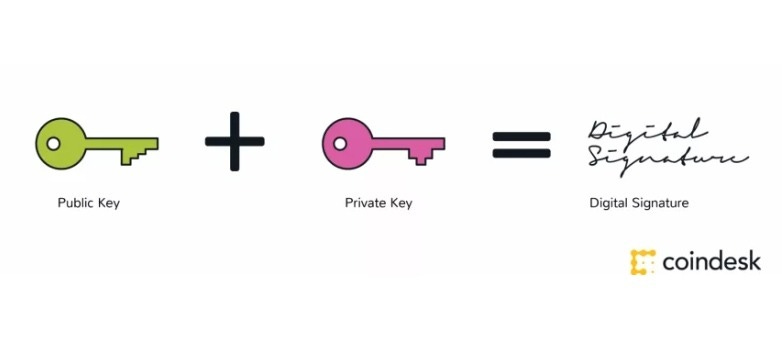

As stated earlier, blockchain is a combination of three technologies. The private key cryptography is concerned with the authentication part of the transaction and this is what secures the transaction. A cryptographic key is a unique set of numbers which is different for every individual or entity. For every financial transaction, the sender needs to be make sure she is sending the money to the right person and the recipient has to know the source of money. Suppose two people, A and B wish to transact on a blockchain based network and A wants to send bitcoin to B. Each one of them has a two cryptographic keys - a public key and a private key. It can be said that a public key like your bank account number which is visible to public and the private key is like your banking password (digital banking) which is accessible to you only, not anyone else. So this combination of a public key and a private key gives every individual a unique digital signature. When A is sending money to B, then B’s public key which is visible to anyone, allows A to securely identify B and make sure the bitcoin is sent to the right person and B can access the this bitcoin sent through the private key. In addition B can also find out the source of bitcoin as A’s public key will be visible to B. This transaction is visible to everyone yet it is highly secured. Thus, the combination of public and private cryptographic keys serves the purpose of creating secure digital identities and provides strong control of ownership over the assets.

Although, the cryptographic keys provide an efficient and accurate way to authenticate a transaction, this is not enough.

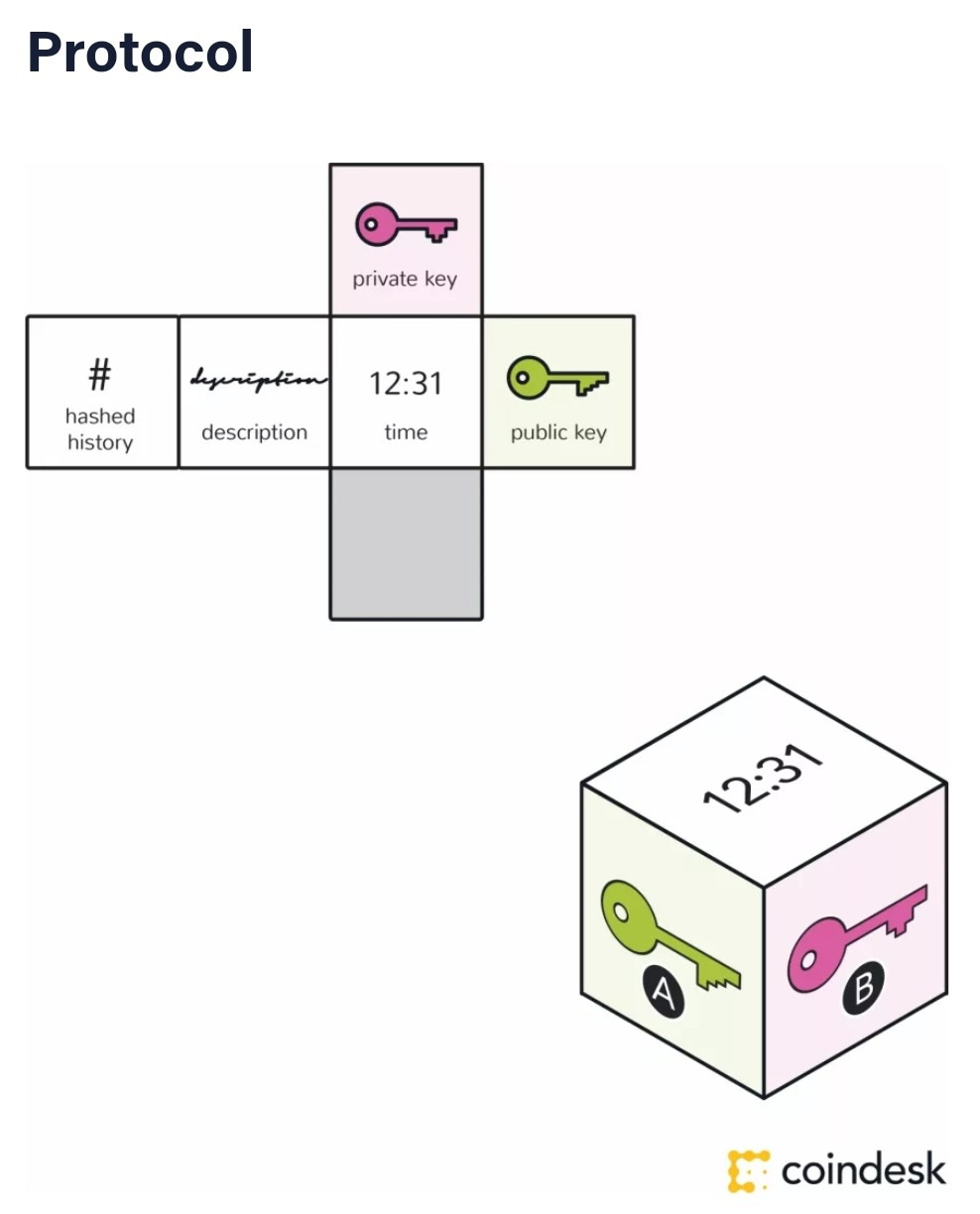

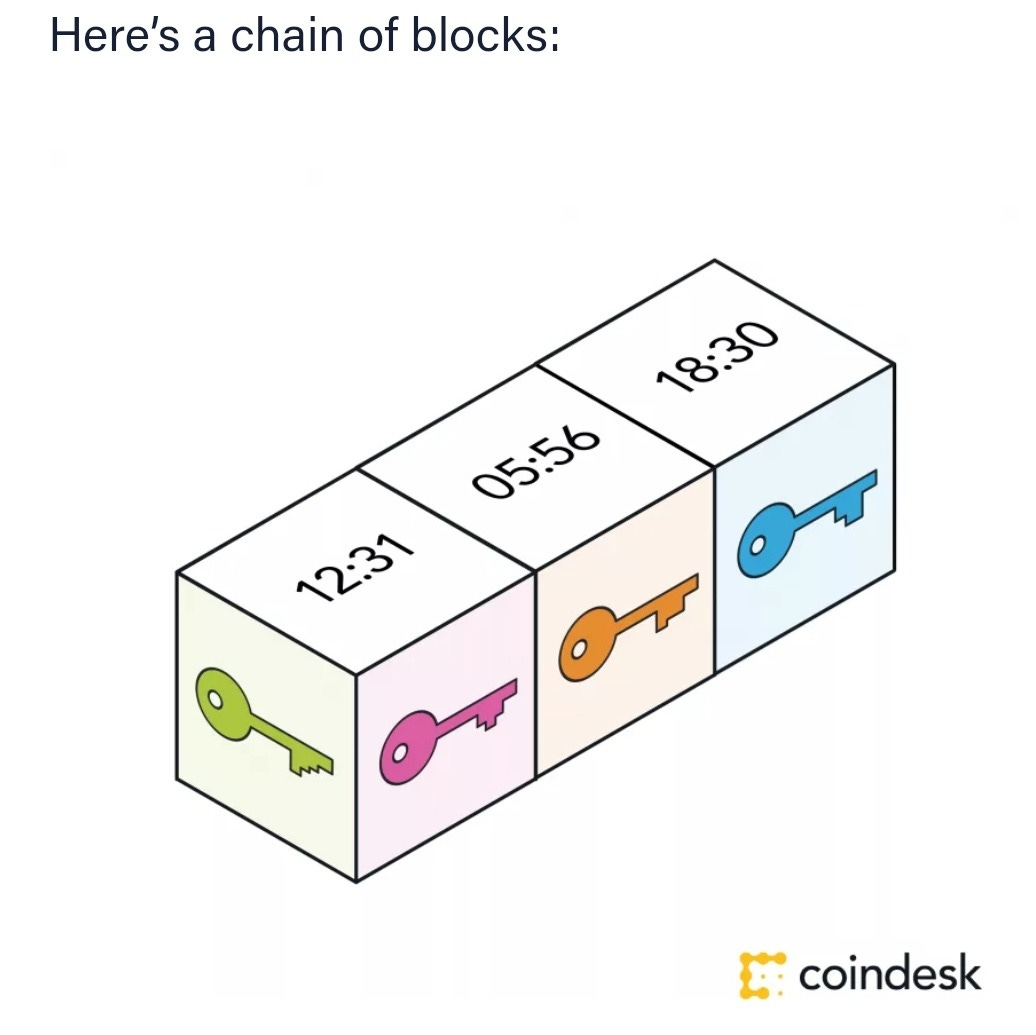

The transaction needs to be authorized. This is where the P2P network comes in which acts like a distributed ledger - a record of all the transactions carried out in the blockchain network, available for everyone to see. Every transaction is recorded in the blockchain. The computers in the network act as validators who arrive at a consensus that they witnessed same transaction at the same time. There is a system of record where every transaction is recorded as a block which contains cryptographic keys, timestamp of the transaction and all the relevant information and data. This block is sent to all the nodes in the network which validate or reject the transaction based on the information available based on the protocol (computer program, discussed further in the article). The network computers authorize the transaction if it is in accordance with the system protocol thus providing legitimacy to the transactions. This verification process is carried out by solving complex mathematical equations or proof of work mathematical problems. This process is irreversible, once the transaction is recorded and marked as legitimate by the computers in the network it cannot be undone. A complete history of transactions is maintained as new blocks are added and a chain of blocks is formed, hence the name blockchain.

So far, it has been established the the major function of validating transactions and and ensuring that the transactions are legitimate is done by the participating computers in the blockchain network architecture. The obvious question any curious person would ask is why would any one give their time and resources to serve the system used by public? This process involves complex mathematical calculations and significant amount of computational power and other resources are required. So why would any one voluntarily help in the functioning of the system? Answer: Incentive based protocol. The protocol is a computer program which basically governs the blockchain network. The computers which serve the network are rewarded. The open or public blockchains this process is called mining. The computers which serve the network are called miners. All the functions listed above which these minors perform are driven by self-interest. Hence, it can be said that a currency is actually inherent in the functioning of a blockchain and is a by-product of the process even if it is being used for other purposes (yes, there are other use cases of this technology) as the miners need an incentive to perform the function of the system. The type and amount of verification also depends on the protocol. The factors which make a transaction valid or invalid, validity checks for new blocks depends on the protocol of the particular blockchain network. The verification process, validation methods and incentives for performing the system functions are all determined by the protocol which is different for every blockchain. Thus, the process for verifying a bitcoin transaction will be different from the process for verifying an ethereum transaction and incentives for bitcoin mining and ethereum mining too will be different.

It is important to note that all the hard work done by the computers participating in the network is driven by self-interest and with the expectation of a lucrative incentive, like Bitcoin or Ethereum. Thus, the greed of individuals is used to serve the public need. Why this works? The answer to this question is given by an ancient economics problem - Tragedy of the Commons. It is a special economics problem when individuals act out of self-interest even if it harms the public. The greed and pursuit of personal gain triumphs over the well being of the society in the minds of these individuals. The blockchain technology attempts to solve this problem. If you want to read more about the tragedy of the commons and how blockchain overcomes this challenge, here is the link.

What can blockchain do?

Now, what is so revolutionary about this technology? It is a complicated structure which enables storage of information and works as a system of record, sure! But what is all the hype about? Decentralization. Think about it, suppose you need money and you decide to borrow from a friend. You ask your friend for a loan and your generous friend agrees to it. He lends you a small amount of money in cash. Now, is this a transaction between two parties? Technically, no. The transfer of value here is cash which is issued by a central bank. Hence, your trust that your friend has given you some valuable currency is based on the fact that the respective central bank considers that to be the case and the citizens of that nation are legally bound to accept it as transfer of value. In a cryptocurrency transaction the two transacting parties just agree that there is transfer of value and this transaction is validated by a number of computers in the network in accordance with the protocol (computer program) of the system. This is decentralization and that is what makes this technology special - it is independent from any central control.

Blockchain is a new technology and a lot is yet to be discovered. It is still in the experimentation phase. Obviously, its not perfect but for sure it will have a huge impact on our lives in future. In addition to facilitating digitally secure yet transparent transactions, it also works as a platform. Cryptocurrency is the first application developed on blockchain platform but there are many other possible platforms like smart contracts, property records, healthcare data storage, banking and finance. To explain, how blockchain can be used in these fields deserves a separate post. The subsequent posts will cover similar topics with an aim to provide more insights on cryptocurrency and other related domains.

That’s all for today folks. Hope you enjoyed this long read. If yes, then please share this post. Also, suggest any other topics or trends you would like to read about in the next posts. Subscribe to The Metro if you are not a subscriber.

DISCLAIMER: All the content on finance, business and financial markets is purely for information purposes and is not any kind of trade or investment recommendation.

Sources: Coindesk, Investopedia

Image Source: Wikipedia, Coindesk, Investopedia